.webp)

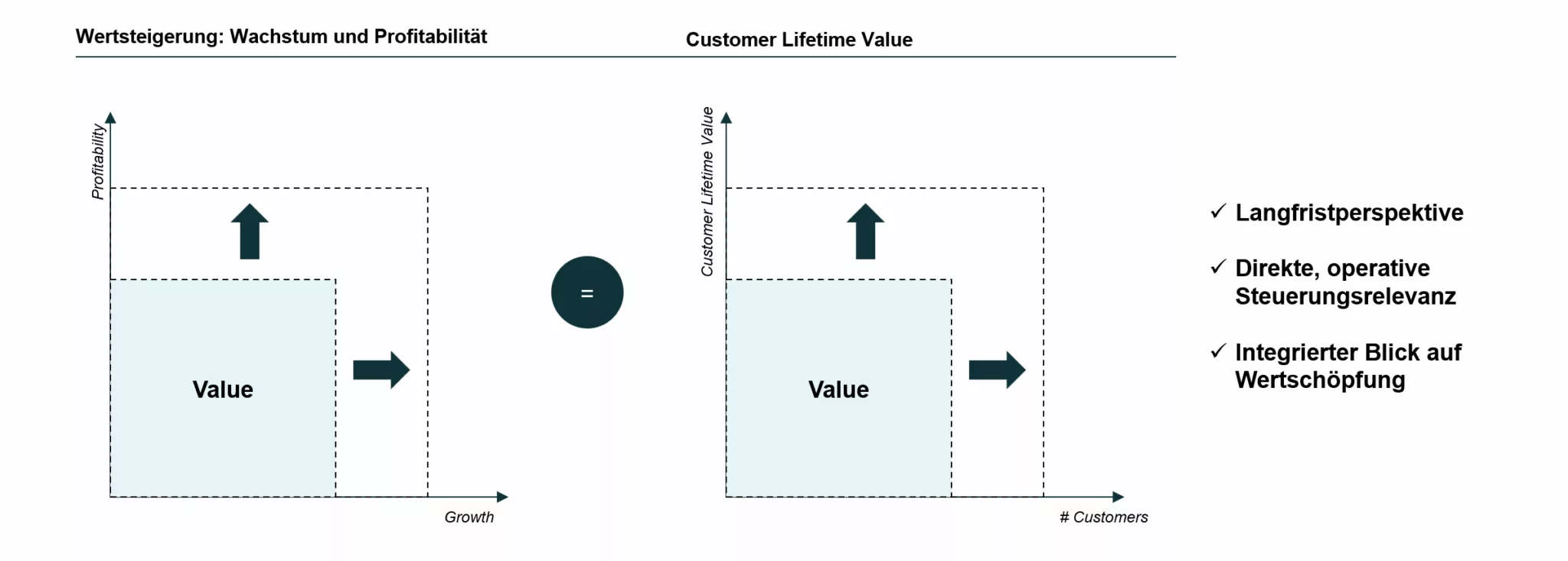

Customer lifetime value (CLV) is the profit contribution a customer generates across the whole relationship, from the cost of winning them to the last renewal. It is the one steering metric that holds acquisition cost, monetisation, retention and expansion in a single number, and that is why it explains enterprise value more reliably than revenue growth or margin read on their own.

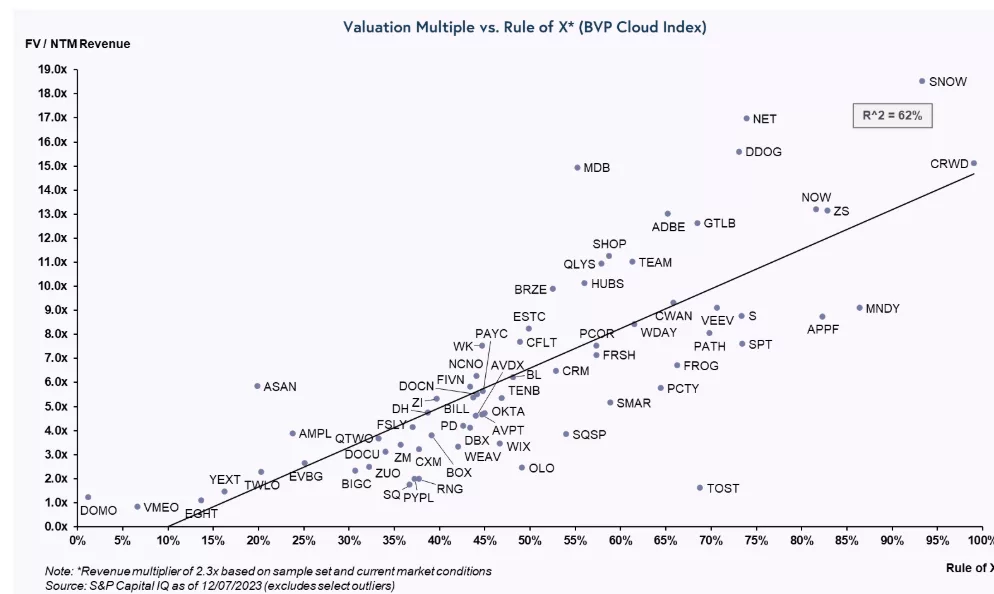

Growth Quality Decides Whether the Multiple Holds

Investors price future cash flows along three dimensions: growth, durability, and risk.

The empirical evidence is clear: growth is valued at a 2-3x higher multiple than profitability at the capital market level (Rule of X, Bessemer Venture Partners).

Aggressive acquisition without matching retention buys revenue that leaves again. Growth bought with price cuts moves the problem into the next period. Both appear as growth in the same line of the income statement, and both erode the durability the multiple is paying for.

So the question for management is which share of the growth is creating value and which share is consuming it.

Source: https://www.bvp.com/atlas/the-rule-of-x

Why the Standard Metric Set Cannot Separate Good Growth

The typical steering metrics - revenue growth, EBITDA margin, CAC, churn rate - reveal symptoms, not drivers. Each sits with a different function, and each gets optimised on its own:

- Marketing optimises CAC - without understanding whether cheaper customers generate less value

- Product optimises features - without detailed transparency into which features drive retention

- Sales optimises deal volume - without measuring which customer segments are profitable

The result: every function optimises its own metric. Nobody optimises overall value. Growth and profitability are treated as a trade-off, not understood as a system.

An integrating logic shows four things the individual metrics cannot:

- How investments in acquisition amortise over the customer lifecycle

- Which customers, segments, and channels actually create value

- Whether growth increases or reduces return on capital

- How unit economics develop at scale

Customer lifetime value closes that gap.

One Comparable Test Across Marketing, Product and Sales

CLV integrates the four dimensions that the standard metrics only capture separately:

- Acquisition - Which customers do we win, at what cost?

- Monetisation - How much value do these customers generate over what period?

- Retention - How long do they stay, and what drives loyalty?

- Expansion - How do we increase the value of existing customers?

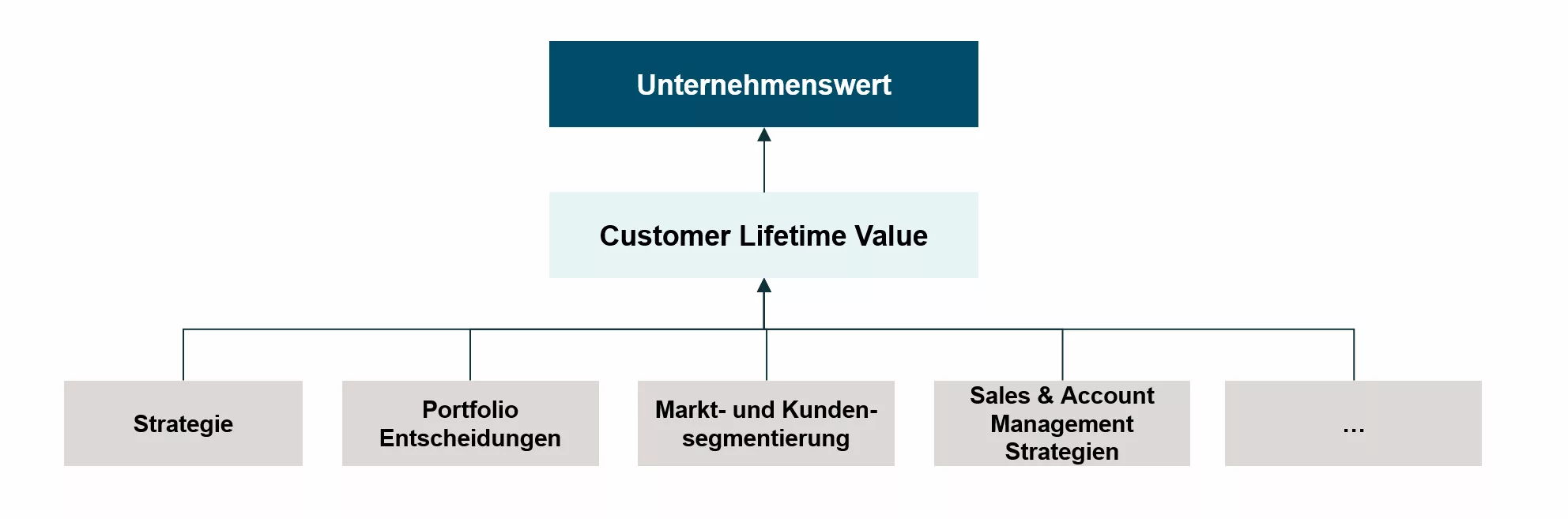

Every investment decision then carries the same test. Does it raise the expected customer lifetime value, and at what cost? That test makes CLV the operational link between strategy and enterprise value. "Sustainable growth" becomes a number with an owner.

What CLV Shows That a Growth Rate Does Not

1. Growth Quality: Value Creation vs. Value Destruction

A growth rate tells you the company got bigger. CLV tells you whether the growth paid for itself.

Two companies growing revenue 50% can sit on opposite sides of value creation:

- Company 1: LTV/CAC = 5:1 - every acquired customer immediately creates value

- Company 2: LTV/CAC = 1.5:1 - growth typically destroys capital, as additional fixed costs, overhead, product development, risk, and cost of capital leave no viable value contribution

Both grow at the same rate. But only Company 1 generates a positive investment cycle: higher CLV allows higher acquisition costs - better channels - better customers - higher retention - even higher CLV. Company 2 runs the same loop in reverse, with falling CLV and rising acquisition pressure.

Growth creates value only on stable or rising customer lifetime values. CLV makes that visible before it reaches the income statement.

2. Scalability: Unit Economics at Expansion

Current margin is a snapshot. CLV by cohort shows which direction the business model is moving in.

Aggregated metrics (70% retention, 58 euros ARPU) hide what the cohorts show:

- Cohort 2020: CLV 125 euros (60% retention, 50 euros ARPU)

- Cohort 2023: CLV 325 euros (80% retention, 65 euros ARPU)

Newer customers are 2.6x more valuable, which means the acquisition and onboarding engine is getting better and the next cohort will pay back faster than the last.

A rising cohort curve justifies a higher multiple, because it shows that scaling adds value instead of diluting it.

3. Forward Perspective: Value Before Accounting Realisation

Traditional metrics are based on historical data or short-term forecasts (12 months). CLV captures value creation across the entire customer lifecycle (3 to 7 years), making value visible before it appears in earnings.

In growing subscription models, acquisition is immediately booked as an expense, while customer value is realised over years:

- Year 1: 1,000 euros revenue, 1,500 euros CAC - 500 euros loss (accounting)

- Years 2 to 5: 5,000 euros lifetime revenue - 4,500 euros lifetime profit (reality)

Earnings-based multiples are often negative or extremely high for growth companies. CLV shows the actual economic value at the point of acquisition.

It also explains the high revenue multiples investors pay on negative earnings. The implicit bet becomes explicit enough to check.

4. Risk Profile: Retention Sets the Discount Rate

Achieved profitability is a fact about the past. CLV is a statement about how long the cash flow lasts.

Example: two companies with identical current EBITDA margins can have fundamentally different risk profiles:

- Company 1: 95% retention - CLV 20,000 euros - 20 years average customer lifetime

- Company 2: 70% retention - CLV 3,333 euros - 3.3 years average customer lifetime

Company 1 can forecast cash flows over two decades with high confidence. Company 2 must continuously re-acquire customers to maintain revenue. This difference in predictability justifies different discount rates - and therefore different valuations - despite identical current profitability.

Retention is the strongest single value driver in the model: an improvement from 90% to 95% doubles CLV, because it compounds across the whole lifecycle instead of adding to it.

What Changes When CLV Runs the Decisions

CLV earns its place in planning only when it decides things. Five decisions change:

Portfolio decisions: New markets are only entered when the expected CLV clearly exceeds acquisition and operating costs - including realistic assumptions on churn and competitive dynamics.

Capital allocation: Budget flows not by function, but by value contribution. A channel with 500 euros CAC and 95% retention (CLV 20,000 euros) beats a channel with 200 euros CAC and 70% retention (CLV 3,333 euros), despite four times higher acquisition costs.

Customer segmentation: The organisation stops treating all customers equally. High-value segments with CLV of 20,000 euros and above are prioritised for acquisition - even at 1,000 euros or more CAC. Low-value segments with CLV of 2,000 euros are deliberately not pursued.

Product decisions: A feature that increases ARPU by 10% but reduces retention from 90% to 85% reduces CLV by more than 25% and is not built.

Process efficiencies: Breaking down CLV into its operational drivers - such as the contribution of procurement, production, and sales - helps optimise processes and directly link process logic with value creation logic.

Why High-CLV Companies Survive a Downturn

Companies with high CLV are less dependent on continuous new customer acquisition. They can absorb a bad year because the cash flow comes from customers already on the books rather than from a monthly intake that has to be replaced.

Deep Dives: The Metrics That Make Up a CLV Model

Calculating and segmenting CLV

- How to Calculate Customer Lifetime Value

- CLV Segmentation: Why One Lifetime Value Number Misleads

- Customer Lifetime Value Benchmarks by Segment

Acquisition economics

- Fully-Loaded CAC: The Acquisition Cost Most Companies Understate

- The LTV:CAC Ratio Is Bimodal Now

- The SaaS Magic Number: A Sharper Read on Sales Efficiency

Retention and cohorts

- Net Revenue Retention: Why the Median Is a Trap

- Gross vs Net Revenue Retention: What GRR Exposes

- Cohort Analysis: How to Read a Retention Curve

- Retention Curve: What Its Shape Says About Product-Market Fit

Where to Start if CLV Is Not Yet in Your Steering

Three questions test whether CLV steers anything or only gets reported:

- Does a CLV figure exist per segment and per cohort, with a named owner? Or only as an average across all customers?

- When acquisition budget is set, does the split follow expected lifetime value? Or last year's channel split?

- Can you show an investor that newer cohorts are worth more than older ones?

One no means the number is being produced rather than used.

Customer Lifetime Value: The Questions We Get Asked Most

What is customer lifetime value (CLV)?

CLV is the profit contribution a single customer generates over the entire relationship, from acquisition through every renewal and expansion to churn. It combines four things that are usually measured separately: what the customer cost to win, what they pay, how long they stay, and how much their spend grows.

How is customer lifetime value calculated?

At its simplest, average contribution margin per period multiplied by expected customer lifetime, discounted if the horizon runs several years. The work sits in the inputs: retention belongs in cohort data rather than an aggregate churn rate, and acquisition cost has to be fully loaded before the ratio means anything. Definitions differ on whether CAC is subtracted, so fix that before comparing numbers.

Why does retention have such a large effect on CLV?

Retention compounds. It sets how many periods the contribution margin is earned across. So it multiplies rather than adds. As set out above, moving retention from 90% to 95% doubles CLV, and the same mechanism explains why two companies with identical EBITDA margins can carry very different risk profiles and therefore very different multiples.

How does CLV affect company valuation?

Through the discount rate and through the multiple. A long average customer lifetime narrows the uncertainty around the outer years of a forecast, which lowers the rate those years get discounted at. Cohorts that outperform the ones before them do the other half: they show that scale lifts the unit economics, and that is what a premium multiple is priced on.

What decisions does a CLV model actually change?

Market entry, because expected CLV has to clear acquisition and operating cost before a market is opened. Budget allocation, because spend follows value contribution instead of function. Segment prioritisation, because high-value segments justify higher acquisition cost while low-value segments are deliberately left alone. And product scope, because a feature that lifts ARPU but costs retention gets rejected.